What do banking customers care about?

Money!

More specifically, your customers care about their money-saving, investing, and earning more. Getting great deals on large purchases – home mortgages and auto loans. You know, the stuff that matters to them. The answer is obvious.

So why do financial services institutions share content like this?

Don’t misunderstand; this content is important.

This content is important to Bank of America (BoA), the beneficiaries of this program, and BoA shareholders. What about their customers? How is this beneficial to them?

That’s the problem; it isn’t beneficial.

The state of online banking today

Competition in the online banking landscape has intensified.

According to Insider Intelligence, “there will be more than 200 million digital banking users in the US by 2022.” Here’s the interesting part about all of this.

“According to data from iResearch Services, more than 90% of people over the age of 60 used online banking for the first time during the pandemic, highlighting the importance of banks getting digital banking right in 2021.” It’s more important than ever that financial institutions get banking just right.

What does this mean?

We’re in the middle of a boom that’s quietly reshaping the banking landscape.

Here, see for yourself.

Source: Insider Intelligence

This is a disaster.

But how? Isn’t banking penetration a good thing for financial institutions? It would be if incumbent financial institutions were ready for it. Research from Oliver Wyman shows that the Rise of Banking-as-a-Service is here, but financial institutions are not ready for it.

“The threat to incumbent financial institutions. This opportunity comes as financial services incumbents struggle with low performance. Together, banking and insurance have been generating lower returns on assets than other industries over the past decade: just 0.8 percent in 2019, compared to 5.7 percent for communication services.

One reason is that incumbent financial institutions are not using their technological assets as efficiently as they could and find it difficult to reduce the cost of technology.”

Here are the challenges outlined in their report.

- Nimble digital-only challengers: “A wave of digital challenger banks are now running at a fraction of the cost of incumbents. Some of these technology companies have obtained banking licenses, enabling them to offer their BaaS platforms to distributors that want to provide financial products to their customers.”

- Non-financial competitors: Technology companies have obtained banking licenses, and non-financial service companies have digitized their offerings, embedding their financial products in other digital platforms (e.g., taking out a loan while checking out during an eCommerce transaction).

- Modular financial services: These companies offer a limited set of unbundled financial services at a significantly lower cost. Identity verification services processing Know your Customer (KYC) applications at a fraction of the cost is another example of specialized players eroding incumbent financial institutions’ competitive advantage and value proposition.

- Google: The search giant continues encroaching into the space, creating content that keeps searchers on their search results pages for longer periods. Rich snippets mean organic content from financial institutions will be buried deeper and deeper in the search results.

What does this mean?

The position of incumbents is far from safe.

This is the cutthroat environment financial institutions deal with on a daily basis. If you’re not on top of your audience research, you don’t even know where to start.

Where is this battle fought?

Read More: Recession Proof: Your SEO Playbook in Economic Uncertainty

Google Search result competition for financial institutions

These battles are happening in Google search results, taking place across several different channels in and outside of Google.

Local search:

As the channel suggests, these are local search queries with clear local intent. These keywords are important battlegrounds for brick-and-mortar banks as they provide customers with the in-person service they’re looking for. Here are a few examples of those queries:

Institution oriented queries

- Banks near me

- Banks near [city]

- Banks near [city, state]

- Banks near [zipcode]

- [Brand] near me

- [Brand] near [city]

- [Brand] near [city, state]

- [Brand] near [zipcode]

This is relevant for branches + ATMs, branches, and ATM-only locations.

Title-oriented queries

- [Mortgage brokers] near me

- [Mortgage brokers] near me

- [Mortgage brokers] near [city]

- [Mortgage brokers] near [city, state]

- [Mortgage brokers] near [zipcode]

Titles include loan officer, investment banker, credit specialist, etc.

Service-oriented queries

- [Personal loans] near me

- [Personal loans] near me bad credit

- [Personal loans] near me no credit

- [Personal loans] near me open now

- [Personal loans] near [city]

- [Personal loans] near [city, state]

- [Personal loans] near [zipcode]

Services run the gamut of your offerings, e.g., refi, refinance, HELOC, home equity line of credit, mortgages, insurance, etc.

Organic search:

These queries move all along the buyer’s journey like any other industry. Financial institutions use educational, navigational, and transactional queries to draw searchers to their sites. Here’s an example of these queries.

Competition oriented queries

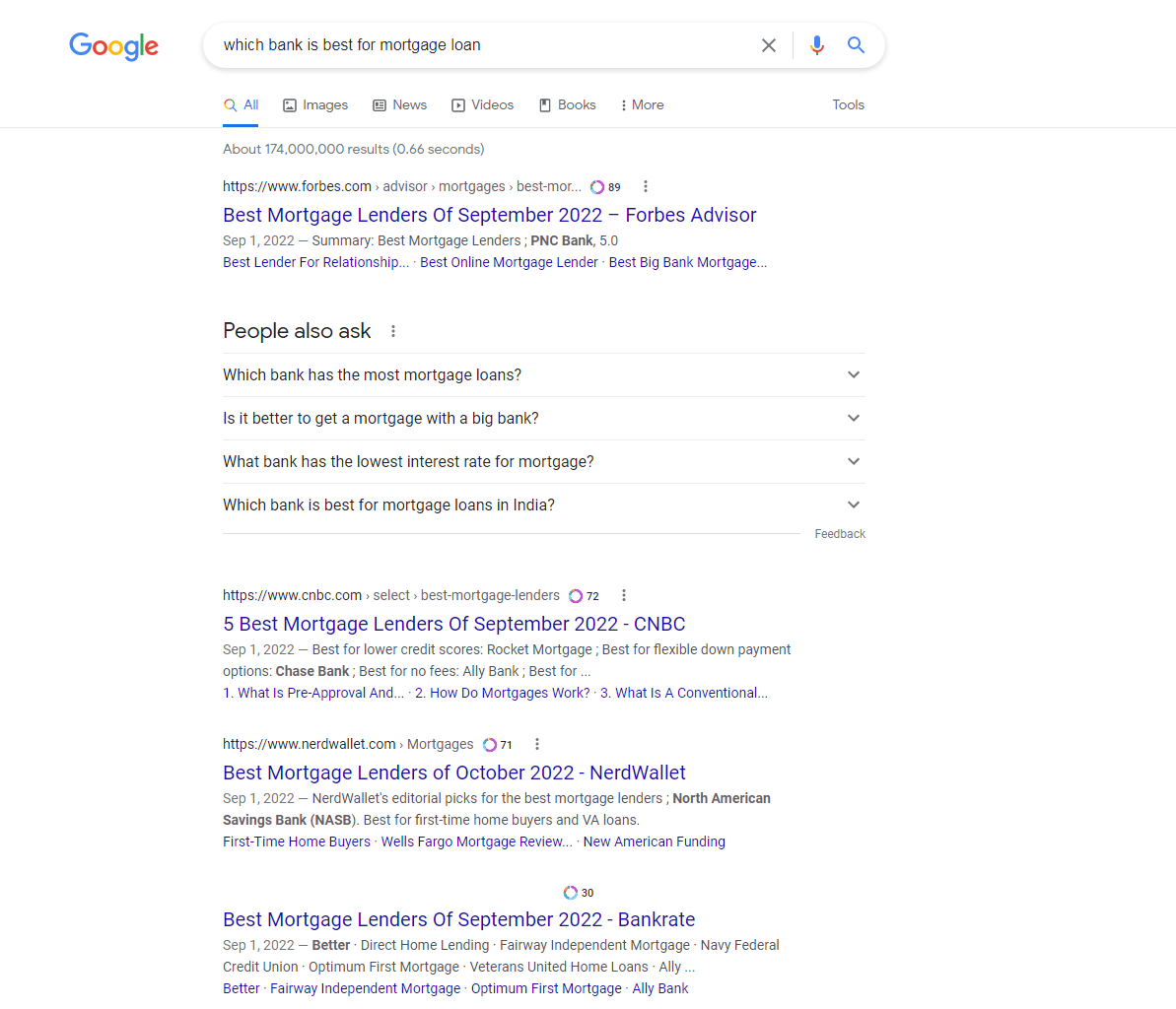

- Which bank is [best] for [refinancing]?

- [Best] [cash-out refinance] companies

- [Consumer reports] [best] mortgage refinance companies

- [Best] mortgage lenders

- [Best] mortgage lenders for bad credit

- [Best] mortgage lenders for no credit

- What bank has the [cheapest] mortgage rates?

- Is [4%] a high-interest rate for mortgages?

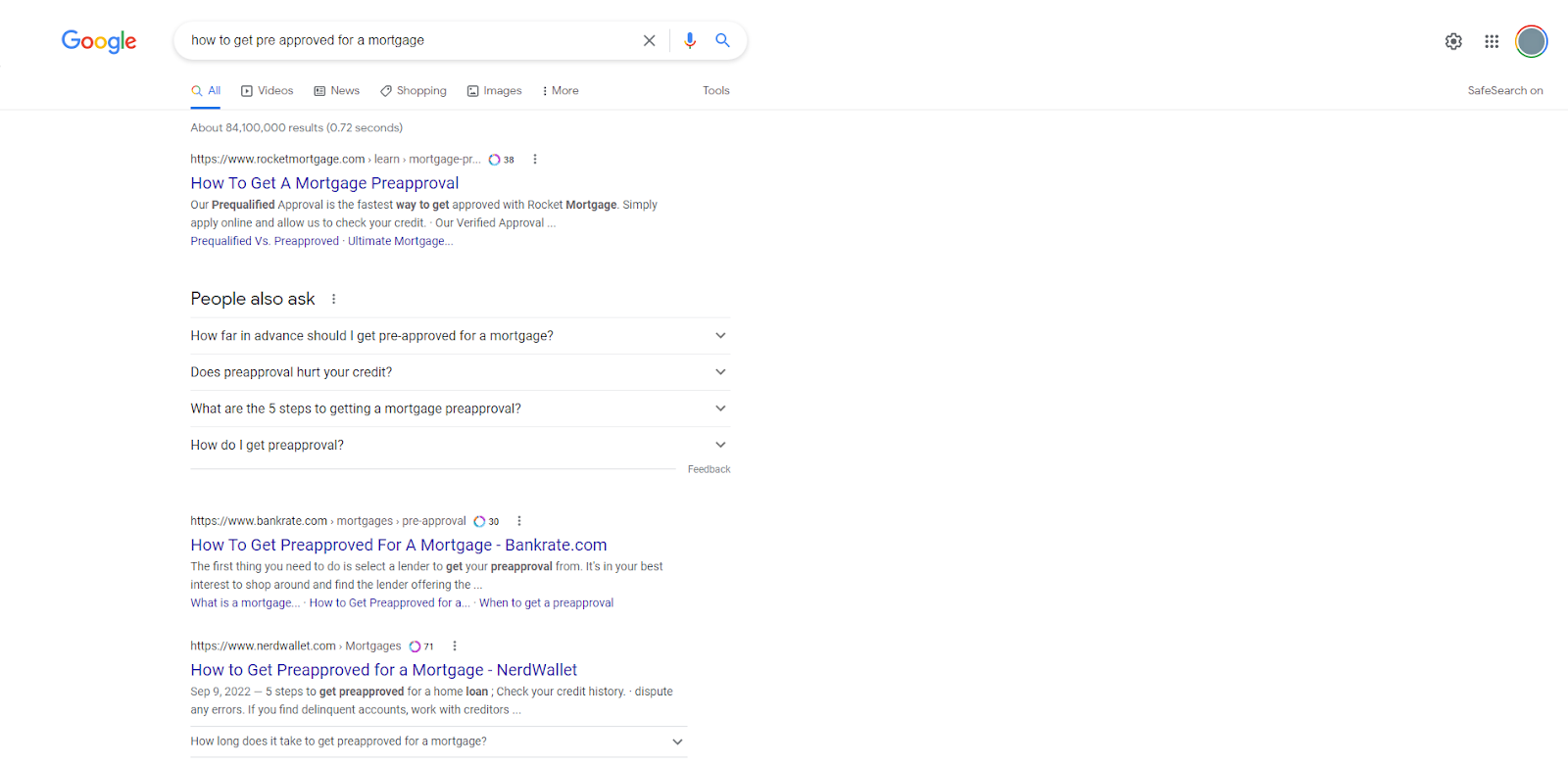

Informational queries

- How to get pre-approved for a mortgage

- Does getting pre-approved for mortgage affect credit?

- What credit score do you need to get pre-approved for a house?

- How far in advance should I get pre-approved for a mortgage?

- Pre-approval mortgage calculator

- Chances of getting denied after pre-approval

- How to increase mortgage pre-approval amount

- What are today’s [refi] interest rates?

- Are interest rates higher for [refinancing]?

- Who pays most of the closing costs?

- [Bank] bank mortgage rates

- Mortgage rates [Bank]

- [Bank] mortgage rates bad credit

- [Bank] mortgage rates subprime

- [Bank] mortgage rates no credit

Commercial queries

- [Bank] bank pros and cons

- [Bank] complaints

- [Bank] reviews

- [Bank] bank employee reviews

- [Bank] bank auto loan reviews

- [Bank] lawsuit

Transactional queries

- [Bank] auto loan

- [Bank] auto loan rates

- [Bank] auto loan payoff

- [Bank] closing costs

As you compete for these queries, you’ll need to maintain incredibly high standards to ensure you’re within Google’s guidelines regarding high E-A-T web pages and YMYL content; make sure you’re following the rules.

What are the rules of engagement for this?

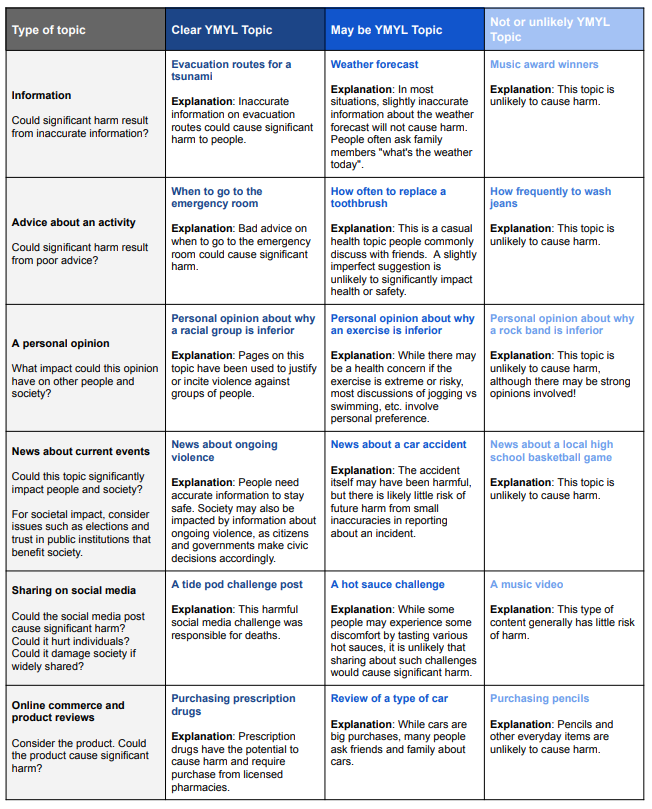

Rules of engagement: Google’s YMYL guidelines for financial institutions

In Google’s Rater’s Guidelines, they begin with the following:

“Some topics have a high risk of harm because content about these topics could significantly impact the health, financial stability, or safety of people, or the welfare or well-being of society. We call these topics ‘Your Money or Your Life’ or YMYL.”

Examples of YMYL pages include:

- News and current events: Content from news organizations covering national/international events, politics, science, etc.

- Civics, government, and law: Civil and legal content that contains information about government, voting, legal issues, social services, etc.

- Finance: Content that discusses financial topics like insurance, investing, taxes, banking, etc.

- Shopping: Content that provides shopping-related content (e.g., specifications, pricing, reviews, etc.) to help people to make purchases online.

- Health and safety: Content covering health and safety topics (e.g., medical issues, drugs, hospitals, injuries, symptoms, conditions, etc.)

- Groups of people: Content discussing specific population segments including, but not limited to, nationality, race, gender, status, etc.

- Other: Content that is not category-specific but still associated broadly with YMYL (e.g., content discussing fitness, nutrition, housing, job hunting, etc.)

Google measures the likelihood of harm to determine if a topic is YMYL.

To determine whether a topic is YMYL, assess the following types of harm that might occur:

- YMYL Health or Safety: Topics that could harm mental, physical, and emotional health or any form of safety, such as physical safety or safety online.

- YMYL Financial Security: Topics that could damage a person’s ability to support themselves and their families.

- YMYL Society: Topics that could negatively impact groups of people, issues of public interest, trust in public institutions, etc.

- YMYL Other: Topics that could hurt people or negatively impact the welfare or well-being of society

So what does this mean?

For starters, Google has very high Page Quality rating standards for YMYL topics. Allowing low-quality pages into their index could harm the health, financial stability, safety, or well-being of the people involved, whether that’s direct or indirect involvement.

Google is absolutely determined to get this right.

Google has been attempting to get this right for several years. They’ve made several updates (e.g., Penguin, the Helpful Content Update) and instituted E-A-T and YMYL guidelines in an attempt to combat low-quality sites. Each update brought Google closer to its goal, making it harder for poor content to achieve visibility.

Your financial institution can use YMYL to win the battle and the war

Competition in the online banking landscape has intensified.

The threat to incumbent financial institutions is severe. This wouldn’t be so bad if incumbent financial institutions were ready for it. As we’ve seen from the research above, many financial institutions are not yet prepared for it.

That’s your opening.

Google looks at several categories, filtering them through its “Do No Harm” YMYL mandate. So what does YMYL mean for finance-related content?

Google wants to see:

- That your content is in full compliance with local, regional, and national regulations (i.e., Gramm Leach and Bliley act)

- That your content displays the appropriate levels of expertise (via credentialed or knowledgeable people) and is authoritative, trustworthy, and credible using a variety of factors discussed here

- That your content adheres to the “Do No Harm” mandates that are part of YMYL

- That your content is thorough, complete, updated regularly, and precise

How do you demonstrate expertise, authoritativeness, and trustworthiness in your content?

- Implement content rebalancing: Odds are you already have a large inventory of content on your site. This means it’s decision time! If you have high-quality pages, you’ll want to determine if you should expand on these high-quality pages and create more pillar and cluster content (that’s oriented around a particular topic. If you have low-quality pages, you’ll need to evaluate whether these pages should be deleted, redirected, or updated and brought up to standard.

- Optimize for the content lifecycle: Your pages will see an eventual decline in performance as traffic wanes and conversions dip. You’ll want to refresh high-quality pages to ensure performance stays high. You’ll need to adjust your content strategy as searcher behavior changes over time. Keep your content up-to-date, and the conversions will continue to flow in.

- Invest heavily in fact-checking: This is already a given for you if you’re part of a financial institution. But it’s doubly important to focus on vetting and assessing the information you put out. Just because it’s accurate today doesn’t mean it will be accurate tomorrow. Content accuracy is an ongoing and neverending effort that will pay dividends with Google.

- Use structured data: Structured data is a straightforward way to increase your website’s search visibility and traffic with JSON-LD, Microdata, and Schema.org markup. Work to earn rich snippets in Google. Remember the competitors I mentioned earlier? Structured data is another chance for you to pull ahead of sneak upstarts looking to steal market share. If you’re a sneaky upstart, it’s even better.

- Optimize utility pages: Make sure Google has indexed the content from your utility pages and that the content is in agreement. It’s easy to add slightly different addresses, phone numbers, and personnel info on your site. Work to ensure it’s consistent on and off-site (i.e., Google My Business). If there are any changes, this needs to be propagated throughout your on and off-site properties.

- Optimize for technical SEO: The technical side of enterprise SEO is a challenge for the enterprise. There’s a tremendous amount of detail that needs to be managed and accounted for. To complicate things further, the departments that need to make changes may not have the access they need to do so. You’ll want to optimize your crawl budget, internal linking, duplicate content errors, soft error pages, site architecture, and more. Take a look at our post for a comprehensive breakdown of these technical SEO challenges (and steps you can take to fix them).

- Address content parity issues: Do search engines see what your searchers see? The knee-jerk answer is ‘of course!’ However, in our research, only 16.29% of the sites we analyzed (5.3 million in total) had word count parity on both desktop and mobile. Here’s why this matters. If mobile visitors see less content than desktop visitors, Googlebot sees less of your content. If Google sees less, you receive less visibility. Conduct parity audits regularly to ensure you get the visibility you’re fighting for.

Your financial institution can win the battle and the war

The threat to incumbent financial institutions is severe. It wouldn’t be so bad if incumbent financial institutions were ready for it. That’s the problem, though, isn’t it? The research shows many financial institutions are not fighting to win the war.

That’s your opening.

Your customers are worried about money matters. More specifically, your customers care about their money-saving, investing, and earning more of it. Getting great deals on large purchases – home mortgages and auto loans. Google wants to see high E-A-T content that does no harm. Your industry is part of Google’s YMYL category.

Both want the same thing.

Treat content as the battleground for your customer’s hearts and minds. Give Google and searchers the content they need, and you’ll dominate the battles and win the war.